Urgent care centers are one of the most convenient ways to get medical treatment for minor injuries, infections, or sudden illnesses. But many patients still wonder: How much is urgent care with insurance? The answer depends on your co-pay, deductible, and type of health coverage.

On average, urgent care visits with insurance cost between $20 and $75 — but in some cases, you may pay $0 if your plan includes full coverage. However, if your deductible hasn’t been met, you might pay more than expected.

Let’s break down how health insurance affects urgent care costs so you always know what to expect before walking in. You can also read here about urgent care cost without insurance.

Typical Co-Pay and Deductible Ranges

Most insurance companies treat urgent care visits differently than regular doctor appointments. Instead of percentage-based billing, you’ll usually pay a fixed co-pay.

| Insurance Type | Expected Urgent Care Co-Pay |

| Medicaid | $0 – $25 |

| HMO / Employer Health Plan | $20 – $50 |

| PPO Plan (Unmet Deductible) | $75 – $150 |

| High-Deductible Plan | Full cost until deductible is met |

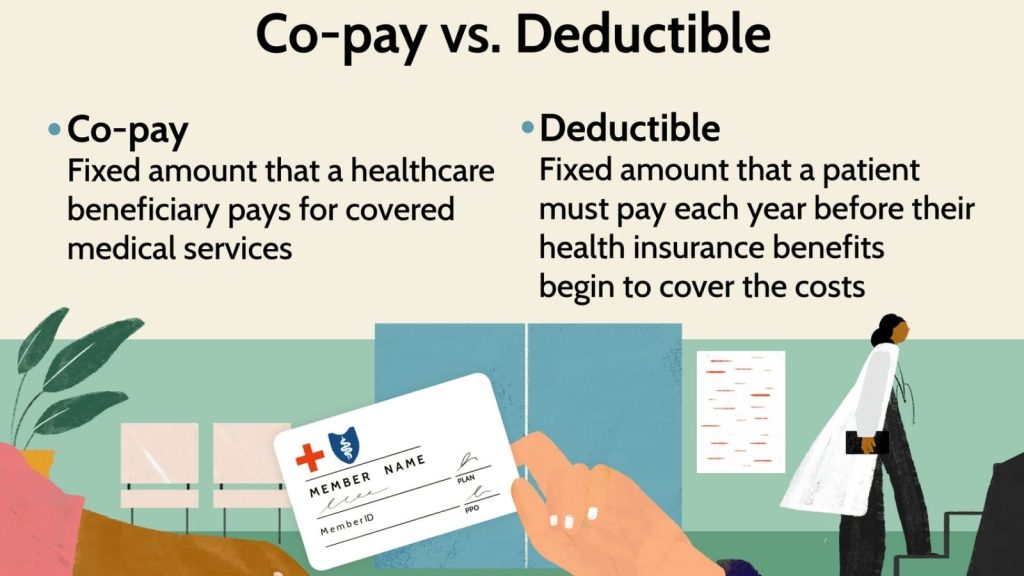

Co-Pay vs. Deductible — What’s the Difference?

- Co-Pay: A flat fee you pay per visit (e.g., $40 per urgent care trip).

- Deductible: The total amount you must pay out-of-pocket before insurance starts covering a higher percentage.

To compare in-network vs out-of-network clinics, check our urgent care cost with insurance comparison

If your deductible is already met for the year, your urgent care bill may be fully or mostly covered.

Insurance Plans That Fully or Partially Cover Urgent Care

Not all health insurance policies treat urgent care the same. Here’s how major plan types compare:

| Plan Type | Urgent Care Coverage |

| HMO (Health Maintenance Organization) | Low co-pay but must visit in-network clinics |

| PPO (Preferred Provider Organization) | More flexibility, but higher out-of-pocket if deductible isn’t met |

| Medicaid & Medicare | Often covers urgent care at minimal cost |

| Short-Term or Limited Insurance Plans | May exclude urgent care entirely — check before going |

Good news: Many employer insurance plans and ACA marketplace plans include urgent care as an essential benefit, making it more affordable than the ER.

For detailed insurance rate breakdowns, see our urgent care cost comparison page.

What to Ask Your Provider Before Visiting Urgent Care

To avoid unexpected billing, call your insurance or check your plan portal and ask:

“What is my urgent care co-pay?”

“Do I need to meet my deductible first?”

“Which urgent care centers are in-network?”

“Does my insurance cover lab tests or X-rays separately?”

Even a 2-minute phone call can save you hundreds of dollars in surprise charges.

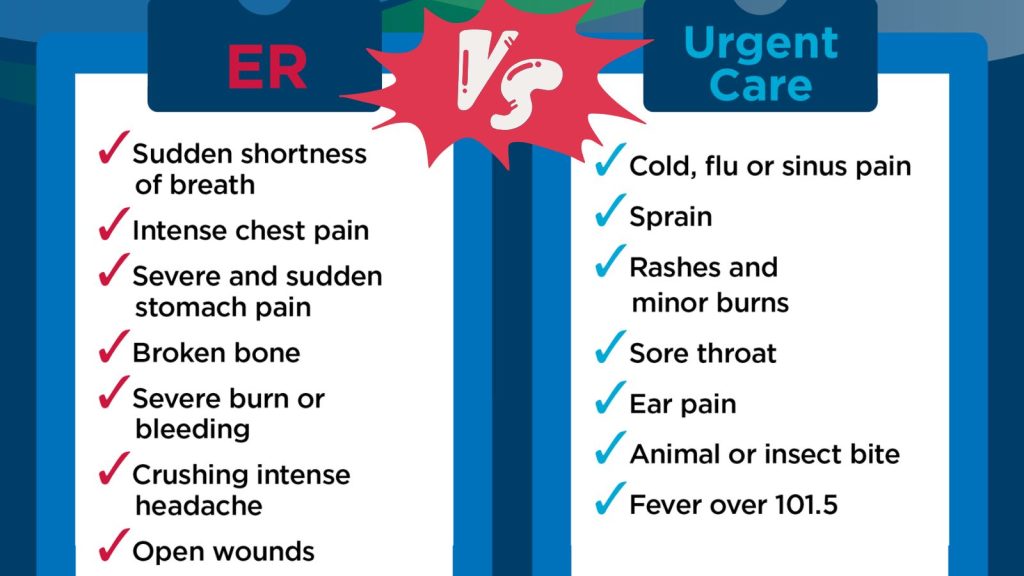

When Is Urgent Care Better Than the ER (Even with Insurance)?

Many people assume the ER is covered more generously under insurance — but that’s not always true. Most insurance providers classify unnecessary ER visits as “non-emergency use,” which can lead to $500+ co-pays.

Go to urgent care for:

- Fever, cough, flu, or infections

- Minor cuts, burns, or sprains

- Allergic reactions without breathing issues

Reserve ER visits for:

- Chest pain or shortness of breath

- Severe head injury or loss of consciousness

- Heavy bleeding or broken bones

Tips to Lower Urgent Care Costs with Insurance

- Choose an in-network clinic only. Out-of-network urgent care facilities can bill 2× more.

- Look up your co-pay before you go.

- Use telehealth first if symptoms are mild. Many insurance plans offer $0 virtual urgent care calls.

- Ask for itemized billing — sometimes clinics add tests you didn’t request.

Frequently Asked Questions (FAQs)

1. Is urgent care covered by insurance?

Yes, most major health insurance plans cover urgent care as part of essential medical benefits, but co-pays and deductibles vary.

2. How much is urgent care with insurance?

The average insured patient pays $20–$75 per visit, depending on plan type and network status.

3. Does urgent care take insurance without a card?

Most clinics can verify eligibility using your name, date of birth, or member ID, but having your card speeds up the process.

4. Can I refuse extra services like X-rays to lower my bill?

Yes, unless medically necessary. Patients have the right to approve or decline additional testing.

5. Will urgent care send a bill later even if I paid co-pay?

If your co-pay doesn’t cover full charges (like lab work), you might receive an additional bill after claim processing.

Final Thoughts

Urgent care is far more affordable with insurance than paying out-of-pocket — but understanding your co-pay, deductible, and in-network rules is essential to avoid surprise costs. With a quick plan check and smart clinic selection, you can get quality care without breaking the bank.